Simple Summary

Risk Parameters

A proposal to adjust 5 risk parameters:

| Risk Parameter | Current Value | Recommended Value |

|---|---|---|

| ETH Collateral Factor | 75% | 78% |

| cbETH Collateral Factor | 73% | 75% |

| DAI Collateral Factors | 80% | 82% |

| USDbC Supply Cap | 40,000,000 | 20,000,000 |

| USDbC Borrow Cap | 32,000,000 | 16,000,000 |

Gauntlet is not recommending any USDbC CF changes until USDC market has been initialized and there is a discussion within the community on next steps for the USDC bridge market.

IR Parameters

Gauntlet recommends adjusting all stablecoin’s Multiplier downwards to incentivize more borrowing and increased utilization of pools. We might withhold this change for USDbC until after USDC markets go live.

| Stablecoin IR Parameters | Current | Recommended |

|---|---|---|

| BASE | 0 | 0 |

| Kink | 0.8 | 0.8 |

| Multiplier | 0.05 | 0.045 |

| Jump Multiplier | 2.5 | 2.5 |

Gauntlet recommends to increase the kink to 80% and Jump Multiplier to 4.8 for the WETH IR curve to improve capital efficency of WETH:

| WETH IR Parameters | Current | Recommended |

|---|---|---|

| BASE | 0.01 | 0.01 |

| Kink | 0.75 | 0.8 |

| Multiplier | 0.04 | 0.04 |

| Jump Multiplier | 3.8 | 4.8 |

Rationale:

Risk Parameters

Our recommendations have an estimated VaR at $0 and LaR at $942k. Based on simulation results, Gauntlet recommends increasing the collateral factors for DAI, cbETH, and WETH in order to improve capital efficiency with minimal impact to risk.

DAI’s has the lowest collateral usage amongst assets in Moonwell BASE with $720k. DAI’s largest supplier represents 75% of DAI supply balances and does not have any open borrow position at this time. We will keep monitoring this position:

DAI’s Largest User Supply Position

With an average collateralization ratio of 2.09% and a collateral usage of $1.66M, WETH’s metrics favor an increase in its CF based on our simulation. The 10% slippage for WETH stands at $3.4M.

cbETH’s collateral usage is $1.17M which is 56% lower than cbETH’s 10% slippage. Based on this data and our simulations, we are supportive of increasing cbETH’s collateral factor. The supporting data section reveals that among the top 10, only the leading supplier of cbETH is borrowing ETH. Enhancing capital efficiency through a higher collateral factor, combined with our additional recommendations, should bolster staked yield recursive positions on Moonwell Base.

BASE Liquidity

| Assets | 10% Slippage | 10% Slippage ($) | 25% Slippage | 25% Slippage ($) | Circulating Supply |

|---|---|---|---|---|---|

| WETH | 2,100 | $3,432,009 | 6000 | $9,805,740 | 59,807 |

| USDbC | 3,000,000 | $3,000,000 | 9000000 | $9,000,000 | 114,941,600 |

| DAI | 1,700,000 | $1,700,000 | 2700000 | $2,700,000 | 22,898,951 |

| cbETH | 1,600 | $2,739,200 | 2000 | $3,424,000 | 23,458 |

| USDC | 2,300,000 | $2,300,000 | 2900000 | $2,900,000 | 160,188,094 |

BASE Circulating Tokens and Supply Cap

| Assets | Circulating Supply | Supply Cap | Supply Cap ($) | Supply Bal / Circulating Supply | Supply Cap / Circulating Supply |

|---|---|---|---|---|---|

| WETH | 59,807 | 10,500 | $17,160,045 | 4.85% | 17.56% |

| USDbC | 114,941,600 | 40,000,000 | $40,000,000 | 3.91% | 34.80% |

| DAI | 22,898,951 | 10,000,000 | $10,000,000 | 18.05% | 43.67% |

| cbETH | 23,458 | 4,000 | $6,848,000 | 5.37% | 17.05% |

| USDC | 160,188,094 | 10,000,000 | $10,000,000 | - | - |

Despite the sufficient circulating supply and liquidity of USDbC to back the current supply and borrow caps, Gauntlet recommends lowering these caps. This is in light of the impending introduction of Native USDC and the expected liquidity shift from bridge USDbC to USDC, as stated in Circle’s announcement. For now, we suggest preserving substantial liquidity in the USDbC pool to ensure no disruptions for users.

IR Recommendations

Stablecoin IR curves would reflect the below changes:

| Utilization | Current Borrow APR | Recommended Borrow APR | Current Supply APR | Recommended Supply APR |

|---|---|---|---|---|

| 0% | 0.01% | 0.00% | 0.00% | 0.00% |

| 80% | 4.00% | 3.60% | 2.72% | 2.45% |

| 100% | 54.00% | 53.60% | 45.90% | 45.56% |

Reducing the Multiplier should cut the Borrow APR from 4% to 3.6%, promoting greater activity in the stable liquidity pools. Given the persistently low utilization and the elasticity shown by borrowers, our advice to decrease interest rates aims to stimulate more borrowing.

WETH IR Curve would reflect the below changes:

| Utilization | Current Borrow APR | Recommended Borrow APR | Current Supply APR | Recommended Supply APR |

|---|---|---|---|---|

| 0.0% | 1.00% | 1.00% | 0.00% | 0.00% |

| At Kink | 4.00% | 4.20% | 2.25% | 2.52% |

| 100.00% | 99.00% | 100% | 74.25% | 75% |

Raising the kink to 80% is expected to enhance the ETH pool’s utilization, potentially leading to over $200k additional borrowing if utilization hits 80% with present supply balances. We’ve adjusted the Jump Multiplier upward to ensure the APR remains consistent with the previous curve at full utilization.

By elevating the kink borrow rate by 20 bps and enhancing the gradient towards the Jump Multiplier, we aim to discourage users in the pool from surpassing the kink.

WETH Supply and Borrow Balance

WETH Utilization relative to Supply Balance & Kink

WETH utilization typically hovers around the kink, except during significant fluctuations in supply and borrowable amounts. However, after such intense shifts in the liquidity pool, utilization invariably gravitates back to the kink.

Methodology

This set of parameter updates seeks to maintain the overall risk tolerance of the protocol while making risk trade-offs between specific assets.

Gauntlet’s parameter recommendations are driven by an optimization function that balances 3 core metrics: insolvencies, liquidations, and borrow usage. Parameter recommendations seek to optimize for this objective function. Our agent-based simulations use a wide array of varied input data that changes on a daily basis (including but not limited to asset volatility, asset correlation, asset collateral usage, DEX / CEX liquidity, trading volume, expected market impact of trades, and liquidator behavior). Gauntlet’s simulations tease out complex relationships between these inputs that cannot be simply expressed as heuristics. As such, the input metrics we show below can help understand why some of the param recs have been made but should not be taken as the only reason for recommendation. To learn more about our methodologies, please see the Helpful Links section at the bottom.

Supporting Data

The below figures show trends on key market statistics regarding borrows and utilization that we will continue to monitor:

Top 10 Borrowers’ Aggregate Positions & Borrow Usages

The highest borrow usage position 8f208812 is a recursive position with USDC and DAI.

Top 10 Borrowers’ Entire Supply

Top 10 Borrowers’ Entire Borrows

Utilization Rate of Assets - Timeseries

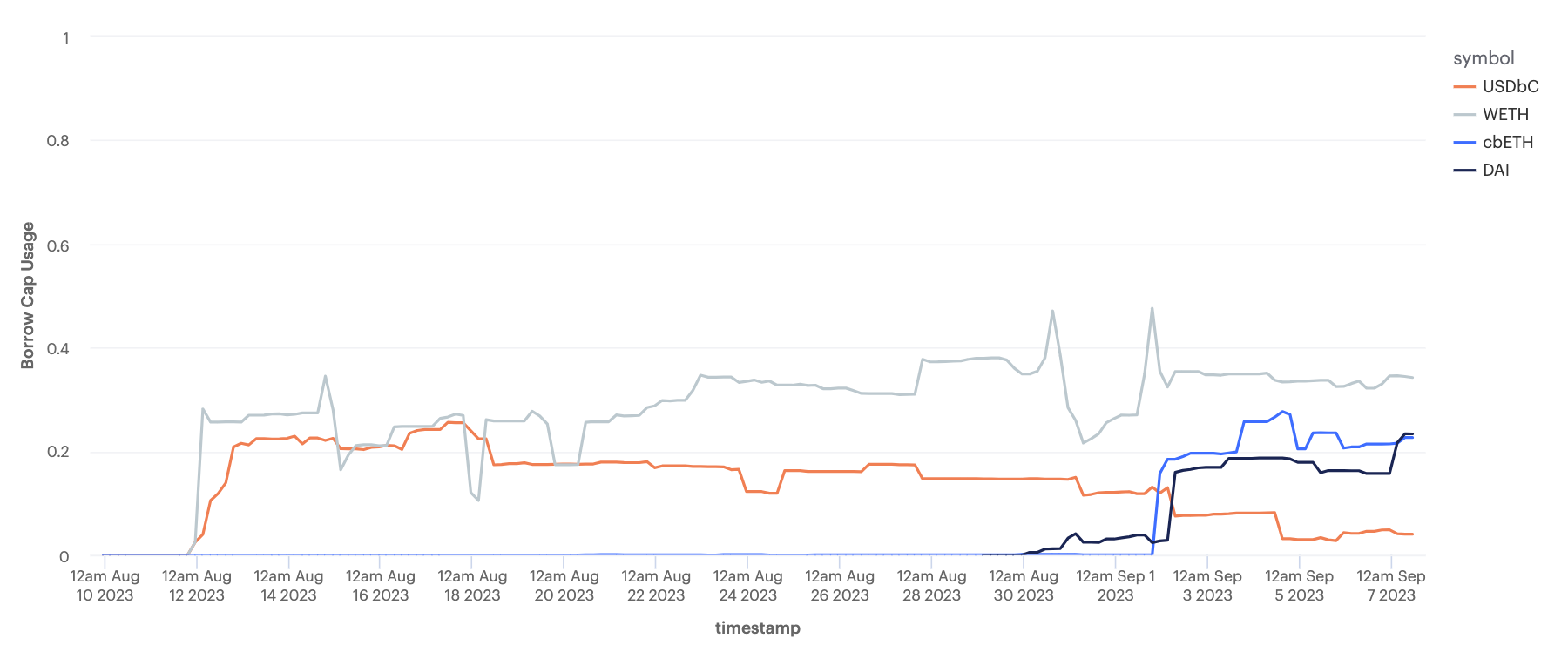

Borrow Cap Utilization

Supply Cap Utilization

We addressed DAI’s full utilization of the Supply cap with Guardian actions. Here is the forum post.

Balances by User Types

Since the last update on the Moonwell BASE market, the percentage of LST Yield Farming Borrow balances increased from les than 1% to 10.42%.

Collateral Usage and Collateralization Ratios

Top Suppliers of cbETH Supply Positions

Top Suppliers of cbETH Borrow Positions

Among the top positions of cbETH, only the highest supply position uses cbETH to borrow additional ETH within the top 10.

Risk Dashboard

The community should use Gauntlet’s Moonwell Base Risk Dashboard to better understand the updated parameter suggestions and general market risk in Moonwell BASE.

Quick Links

Please click below to learn about our methodologies:

Gauntlet Parameter Recommendation Methodology

Gauntlet Model Methodology

By approving this proposal, you agree that any services provided by Gauntlet shall be governed by the terms of service available at gauntlet.network/tos.